AV Market Update CW20

Waymo Production Scale-Up, Uber's global AV strategy & Aurora Q1 Earnings

👋 Hello!

We've had another eventful week behind us with new details about Waymo's manufacturing capabilities, additional Uber partnership announcements, and Aurora's Q1 earnings call.

I found the details about Waymo particularly fascinating this week. To analyze them, I've used Aswath Damodaran's corporate lifecycle framework, which I find extremely valuable for understanding where a company stands in its evolution and what the implications of that position are.

If you enjoy the application of such frameworks for analysis and would like to see more of this approach in future newsletters, please let me know in the comments!

But enough preamble—let's dive in.

Today's newsletter has 3,300 words and takes about 15 minutes to read.

🚗 Waymo's Production Scale-Up and Uber's Global Strategy Signal AV Market's Inflection Point

In Mesa, Arizona, a 239,000-square-foot facility has quietly become the epicenter of Waymo's commercial ambitions. This factory, which opened in October 2024, represents a fundamental shift in Waymo's strategy—it's no longer just refining autonomous technology but building a full-scale mobility business capable of industrial-level production.

What makes this facility significant isn't just its size, but what it signals about Waymo's evolution. After years of keeping fleet details private, Waymo has revealed that its current 1,500 vehicles deliver 250,000 paid rides weekly. That's approximately 24 rides per vehicle per day.

Project this utilization to a future fleet of 10,000 vehicles, and the numbers become staggering: 250,000 rides daily or 1.75 million weekly. At this scale, Waymo would transform into one of America's largest mobility providers, generating potential annual revenue in the billions.

To understand Waymo's position more deeply, I find

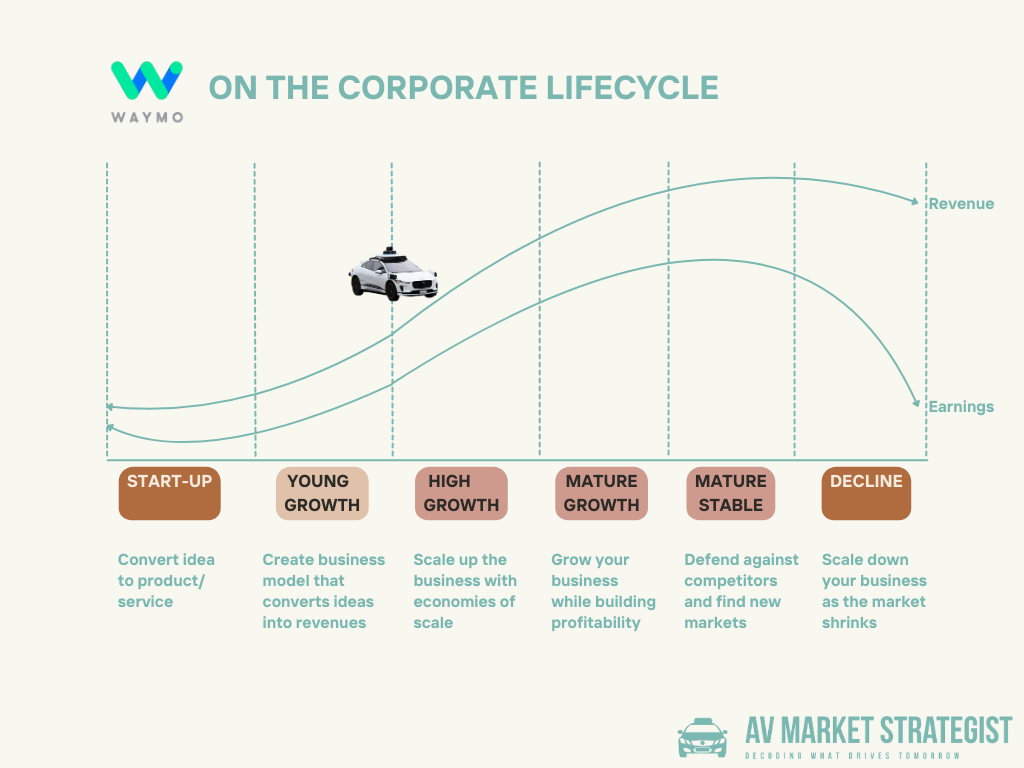

Damodaran's model divides a company's evolution into six distinct stages: Start-Up, Young Growth, High Growth, Mature Growth, Mature Stable, and Decline. Each stage presents unique characteristics, financial profiles, and strategic imperatives:

Source: Aswath Damodaran, Corporate Lifecycle

Start-Up: The idea stage with minimal or no revenues, where a concept is being developed. Cash burn is typically funded by founders, angels, or incubators, with the strategic goal of proving the concept works.

Young Growth: The company has a working product and begins building a business model. Revenues start to appear but losses continue as the company refines its offering. The focus is on establishing product-market fit and developing a viable path to profitability.

High Growth: The scale-up phase with rapid expansion, surging customer growth, and entry into new markets. Revenues grow significantly, though profits might still be modest due to reinvestment. The goal is scaling quickly to capture market share.

Mature Growth: The company is large with more moderate growth as core markets saturate. Revenues rise at a decreasing rate, the company is typically profitable, and strategic goals shift toward extending growth through expansion and acquisitions.

Mature Stable: The steady state with minimal revenue growth, a dominant market position, stable margins, and strong free cash flow. Focus shifts to efficiency and returning capital to investors.

Decline: Characterized by shrinking business, contracting markets, and pressure on profit margins, requiring cost-cutting or business reinvention.

Looking at Waymo's current operations and trajectory, it appears to be in the critical transition phase between Young Growth and High Growth stages.

Several key indicators support this assessment:

Operational Scaling: With 1,500 vehicles delivering 250,000 weekly paid rides and plans to expand to 3,500 vehicles by 2026, Waymo is clearly beyond mere proof of concept (Start-Up) or product-market fit testing (Young Growth). The company is actively scaling its operations with a validated service model.

Financial Profile: Despite growing revenue from rides, Waymo remains in investment mode. In October 2024, it raised $5.6 billion in a funding round led by Alphabet and other investors, valuing the company at approximately $45 billion. This capital infusion pattern suggests a company that has proven its business potential but requires significant investment to reach scale—a classic High Growth stage characteristic.

Geographic Expansion: Waymo's aggressive market entry strategy (Phoenix, San Francisco, Los Angeles, Austin, with Atlanta, Miami, and Washington D.C. planned) reflects a company that has moved beyond testing its business model to rapidly expanding its footprint—another High Growth indicator.

Manufacturing Investment: The establishment of the Mesa factory to produce thousands of vehicles annually signals the transition to scaling operations at an industrial level. This isn't experimental production but preparation for mass deployment.

Vehicle Platform Diversification: Waymo's shift from exclusively using premium Jaguar I-PACEs to incorporating the Hyundai Ioniq 5 and Zeekr RT minivan platforms represents a strategic move to improve unit economics—a classic challenge during the Young Growth to High Growth transition. These newer platforms likely offer lower costs and better fit-for-purpose designs for robotaxi operations, though the Zeekr vehicles face already a significant hurdle with Trump-era tariffs on Chinese EVs now at 145%, up from 100% under Biden.

The transition from Young Growth to High Growth is also evident in how Waymo is increasingly being evaluated by market observers and industry analysts. During its earlier stages, external assessment focused primarily on technology-focused metrics (like disengagements per mile and technical milestones). Now, we're witnessing a significant shift toward operational and economic performance indicators.

Market analysts are increasingly scrutinizing metrics like fleet size, ride volume, geographic footprint, and most critically, fleet utilization rates. This evolution in external evaluation criteria reflects the maturing expectations for Waymo as a business rather than merely a technological experiment.

We can expect more analyses focusing on these operational metrics in the coming months, similar to what analyst Neel Mehta of G2 Ventures recently noted:

"It starts to become a very big deal if they can crack 30 trips/vehicle/day," explaining that at this utilization level, "it's plausible they could recoup the upfront investment on the vehicle in 1 year" even with vehicle costs of $125,000-$150,000.

Investors and analysts are now asking not just "Does the technology work?" but "Can the business model generate returns at scale?"—the quintessential question for companies in the High Growth phase.

The implications of this lifecycle positioning are significant for Waymo's strategic priorities:

Rapid Geographic Expansion: Waymo must carefully pace its city launches to balance market presence against operational capacity. Its phased approach and strategic partnerships (like using the Uber platform in Austin to generate demand) represent attempts to optimize this expansion.

Fleet Growth and Economics: Scaling the fleet while improving economics is paramount. The Mesa factory allows Waymo to control the vehicle integration process, potentially reducing per-unit costs and accelerating deployment. Additionally, maximizing utilization (rides per vehicle per day) is critical to profitability—idle robotaxis generate no revenue.

Technology and Safety Leadership: Even while focusing on scaling operations, Waymo must maintain its technological edge. This includes expanding operational capabilities (like the addition of fully autonomous freeway driving) while ensuring safety standards remain impeccable as the fleet grows.

Ecosystem Development: Building a network of strategic partnerships becomes increasingly important. Waymo's collaboration with automotive manufacturers for vehicle platforms, with Uber for customer acquisition, and with municipal authorities for infrastructure access (like airport pickups) creates an ecosystem that can accelerate adoption.

As Damodaran notes, transitions between lifecycle stages are often the most challenging periods for companies, requiring different leadership skills and strategic frameworks.

For Waymo, successfully navigating this transition means balancing aggressive expansion with developing the operational discipline and financial structures of a more mature business—all while addressing immediate challenges like tariff impacts on its Zeekr vehicle strategy and competition from rivals racing to establish their own market positions.

While Waymo builds its production capacity, Uber is executing a complementary strategy at breathtaking speed: creating a global AV network through strategic partnerships.

In just three weeks, Uber has announced collaborations with Volkswagen and May Mobility in the U.S., Momenta in Europe, and most recently, WeRide and Pony.ai in the Middle East and Europe.

The WeRide partnership is particularly ambitious, with Uber committing an additional $100 million to expand their collaboration from Abu Dhabi (where they already operate) and Dubai to 15 more global cities over the next five years.

Simultaneously, Uber's new partnership with Pony.ai will launch robotaxi service in the Middle East later this year, initially with safety operators before transitioning to fully driverless operations upon regulatory approval.

This flurry of partnerships isn't random—it reveals Uber's deeper strategy to position itself as the global orchestrator of autonomous mobility. By partnering with technology providers across multiple regions, Uber is creating a platform model where it handles marketplace operations, customer acquisition, and routing while AV companies supply the autonomous technology.

Most fascinatingly, these partnerships demonstrate how Uber is becoming the gateway for Chinese AV companies to export their technology globally. Just as China has done with solar panels, EVs, and consumer electronics, autonomous technology is becoming another category Chinese companies are ready to export at scale.

WeRide, Momenta, and Pony.ai have all chosen to partner with Uber rather than build their own consumer brands internationally—a pragmatic choice that trades direct customer relationships for rapid market access and operational scale.

The Austin partnership with Waymo provides a compelling proof point for this model. During Uber's recent earnings call, CEO Dara Khosrowshahi revealed that the 100 Waymo vehicles operating in Austin are "busier than 99% of all drivers" in terms of completed trips per day. This isn't just a promotional statistic—it highlights the fundamental operational advantage AVs have over human drivers.

What makes this statistic so powerful is understanding the comparison point.

According to industry analyst Harry Campbell, top-performing human Uber drivers in Austin complete approximately 160-170 trips weekly, working roughly 80 hours per week at 2 rides per hour. These are the outliers—the most productive 1% of the human driver pool.

Meanwhile, Waymo vehicles in Austin are estimated to be completing 24-30 trips daily. The advantage is structural: AVs don't need sleep, meals, or rest breaks. A Waymo operating 22 hours daily at just one trip per hour would complete 154 weekly trips—nearly matching the most productive human drivers. At two trips per hour, that jumps to 308 weekly trips, completely rewriting the economics of mobility services.

This utilization differential creates a virtuous cycle. Higher utilization means faster capital recovery, which enables more competitive pricing, which increases demand, which improves utilization further. If Uber can consistently push utilization to 30 rides per vehicle daily across its autonomous fleet, the unit economics become compelling even with today's expensive AV hardware.

However, this model creates a delicate balancing act for Uber. As AVs begin to dominate high-demand routes, the company must maintain an equilibrium that keeps human drivers engaged and profitable, particularly during the multi-year transition period when AVs will operate alongside traditional rideshare services.

Uber's partnership strategy reveals another critical insight: the AV revolution will be global from the outset, not dominated by a single player or limited to specific markets.

By partnering with regional technology providers like WeRide (strong in China and the UAE), Pony.ai (established in China and Luxembourg), and Momenta (specialized in China and Europe), Uber is building a network that can adapt to diverse regulatory, cultural, and operational environments.

Europe and the Middle East are emerging as the first international battlegrounds for commercial AV services outside the companies' home markets. These regions offer a combination of regulatory openness, urban density, and economic opportunity that makes them attractive for early deployment.

This approach gives Uber significant strategic leverage. While AV companies focus on perfecting their technology for specific conditions, Uber provides the marketplace infrastructure, customer relationships, and global brand recognition that can accelerate adoption.

AV companies, particularly those from China, appear willing to give up the direct customer interface in exchange for scale, trust, and market access—a pragmatic approach that could accelerate global deployment.

Several critical factors will determine how quickly these developments accelerate:

Vehicle economics: Waymo's sixth-generation hardware arriving later this year promises significant cost reductions, potentially accelerating the path to profitability despite tariff challenges for Chinese-manufactured components

Regulatory approvals: Both Waymo's expansion and Uber's partnership strategy depend on securing permits across diverse jurisdictions—a complex process that varies significantly by region

International dynamics: Uber's partnerships with Chinese AV companies face potential complications from escalating trade tensions, which could impact both cost structures and market access

Consumer adoption: While utilization statistics are promising, long-term success depends on widespread consumer trust and preference for autonomous rides—particularly as safety incidents like Zoox's recent recall demonstrate the ongoing technical challenges

Bottom line: It will be fascinating to watch the AV industry's evolution in the coming months. The most compelling question: How will Waymo navigate the critical transition from Young Growth to High Growth in Damodaran's Corporate Lifecycle model? Can they overcome production challenges, efficiently scale their fleet, and achieve the operational metrics needed to justify the substantial investments?

Simultaneously, Uber faces its own test: can its global orchestrator strategy succeed beyond the US, particularly through partnerships with Chinese AV providers in Europe and the Middle East?

🔗 TechCrunch (1) / TechCrunch (2) / Forbes (1) / Forbes (2) / The Verge / Bloomberg / Investing.com / Driverless Digest / Luxembourg Times

🚚 Aurora's Q1 2025 Earnings

Aurora Innovation's first-quarter 2025 earnings, released just days after completing their first driverless commercial deliveries between Dallas and Houston, provide insights into the economics of autonomous trucking's commercialization phase.

Aurora's Q1 financial picture reflects a company strategically investing to scale operations following its landmark commercial launch. Operating expenses reached $211 million, up from $193 million in Q1 2024. R&D expenses, unsurprisingly, dominated at $182 million (or $153 million excluding stock-based compensation), underscoring the continued technological refinement necessary even after achieving driverless status.

The company's net loss widened to $208 million compared to $165 million in the same quarter last year—an expected pattern as Aurora builds out operational infrastructure to support its growing commercial footprint.

Cash consumption reflected disciplined capital management with $142 million in operating cash burn and $8 million in capital expenditures, leaving the company with a substantial $1.2 billion in liquidity that management projects will fund operations into late 2026.

Perhaps the most intriguing aspect of Aurora's earnings is what isn't immediately obvious on the financial statements: actual revenue.

For investors scanning the reports, revenue appears conspicuously absent. This is because Aurora's pilot revenue—which reached $871,000 this quarter, up 22% quarter-over-quarter—is currently classified as a contra-expense within R&D.

This accounting treatment reflects the company's pre-commercial phase status, but CEO Chris Urmson confirmed that beginning next quarter, Aurora will report revenue officially, combining both driverless revenue and ongoing pilot revenue.

The company's CFO, David Maday, noted during the earnings call that while 2025 revenue is expected to be "modest, in the mid-single-digit millions," the figure should build sequentially throughout the year as operations scale. For investors focused on the path to profitability, this gradual revenue ramp provides tangible metrics to track Aurora's commercial progress.

Aurora's currently operates driverless trucks exclusively during daylight hours and in clear weather conditions—limitations that significantly constrain vehicle utilization and, consequently, revenue potential. However, the company has outlined an ambitious roadmap to remove these constraints in the second half of 2025.

"We'd like to have a high return on asset for every truck that we have, and so we'll try to drive efficiency to get as many miles on as many trucks as fast as possible," Maday explained during the earnings call. "We should be able to double our drive time as soon as we unlock night. And that's our next key milestone."

This operational expansion represents a critical economic inflection point. By extending operations to include night driving and adverse weather conditions (including rain and heavy wind), Aurora can potentially double truck utilization from approximately 8 to 16 hours daily—dramatically improving the unit economics of each vehicle in its fleet.

After successfully launching with a single driverless truck in late April, Aurora has already expanded to two driverless trucks operating daily on the Dallas-Houston corridor. Management projects that its fleet will grow to "tens of trucks" by the end of 2025, strategically deployed across multiple lanes, including a planned expansion to the Fort Worth-El Paso-Phoenix route.

This 1,000+ mile route presents a particularly compelling use case for autonomous trucking, as it exceeds the 11-hour federal hours-of-service limitation for human drivers. By deploying driverless trucks on routes that human drivers cannot complete in a single shift, Aurora can demonstrate one of autonomous trucking's most significant value propositions: the ability to move freight faster and more efficiently on long-haul routes.

Looking Ahead:

Aurora's Q1 2025 results and forward guidance reveal a company whose focus has shifted from proving technological feasibility to demonstrating commercial viability. As CEO Chris Urmson noted in the shareholder letter, "Our focus now turns to proving the promise of the technology, increasing the value of our product for our customers, and ultimately becoming an essential partner in the freight industry."

The company's anticipated progression through 2025 outlines a clear strategy: expand operational capabilities (night driving, adverse weather), extend geographic reach (new lanes), and increase fleet size—all while driving down costs through hardware improvements, including their second-generation kit that promises "a step-function reduction in hardware costs."

For investors, the coming quarters will be critical in evaluating whether Aurora can execute on this strategy and demonstrate improving unit economics. The company's long-term success hinges on its ability to efficiently scale operations while simultaneously reducing costs—the classic growth company challenge.

🔗 TechCrunch / Aurora (1) / Aurora (2) / Seeking Alpha

💡 Quick Takes:

🔄 TractEasy Launches First Level 4 Autonomous Baggage Operations at Kansai Airport

TractEasy and EasyMile have deployed the world's first Level 4 autonomous tow tractor for Ground Support Equipment at Kansai International Airport in Japan. This implementation aims to reduce aircraft-to-baggage return times and address labor shortages in ground handling operations.

🚙 Baidu's Apollo Partners with Car Inc for "First-of-its-Kind" Autonomous Rental Service

Chinese tech giant Baidu's smart driving unit Apollo announced a strategic partnership with local auto rental firm Car Inc to launch what they describe as a "first-of-its-kind" autonomous driving rental service. The agreement signed in Beijing aims to "jointly promote the application of autonomous driving technology" in Chinese cities, potentially creating a new business model that bridges traditional car rentals with autonomous mobility services.

🔗 Reuters

⚠️ Zoox Issues Voluntary Recall After Minor Collision in Las Vegas

Amazon-owned autonomous vehicle company Zoox paused its driverless testing program for over a week and issued a voluntary recall affecting approximately 270 vehicles following a minor collision in Las Vegas on April 8. The incident occurred when a Zoox vehicle inaccurately predicted the movement of a passenger car approaching from a commercial driveway. Despite the setback, Zoox confirmed it still plans to launch commercial robotaxi service in Las Vegas later this year, highlighting the ongoing challenges AV companies face in perfecting prediction algorithms for complex urban environments.

🔗 TechCrunch

🚛 ATLAS-L4 Research Project Successfully Completes Autonomous Truck Development

A consortium of twelve partners from industry and academia has successfully completed the ATLAS-L4 project, developing an autonomous truck for hub-to-hub transport on German motorways. The €59.1 million initiative, funded by the Federal Ministry for Economic Affairs and Climate Protection, achieved the first-ever Level 4 test approval for a commercial vehicle in Germany.

🔗 MAN

📚 Worth Reading

Harry Campbell's Analysis: Waymo-Uber Austin Utilization

Industry analyst

provides essential context for understanding Uber CEO's statement that Waymo vehicles in Austin are "busier than 99% of all drivers."🔗 The Driverless Digest

📊 Weekly Performance

Note: Stock performance data as of May 11, 2025. Past performance does not indicate future returns.

Thanks for reading!

If you found value in this newsletter, please consider sharing it with a friend or colleague who might benefit from these insights.

And if you haven't already, subscribe to stay updated on the latest developments in the autonomous driving industry.